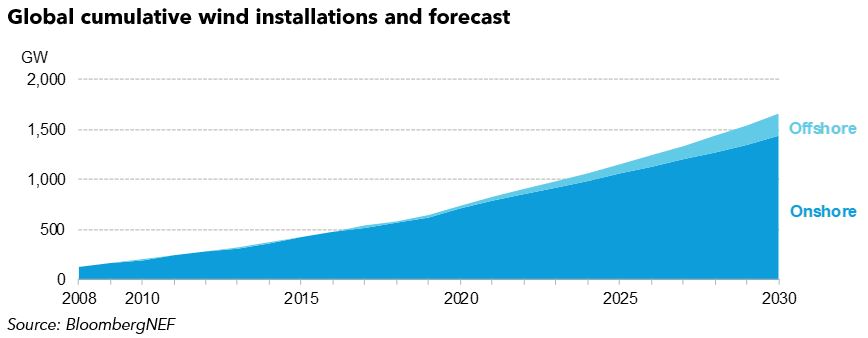

The wind sector brushed off the effects of Covid-19 in 2020 to install 97GW, smashing the previous record set for annual installations in 2015 by over 30GW. The industry is set to see tremendous growth over the coming decade. We predict cumulative wind capacity could double from 2021 to 2030, reaching 1.7TW.

The wind supply chain proves its strength

The wind supply chain proves its strength

Last year’s installation record was primarily driven by highest-ever onshore wind addition in the world’s two largest markets: the U.S. and China. The final result was an installation total that many – including BNEF – predicted was impossible and illustrates just how much supply chains can flex when there are subsidies on the line.

In China, the onshore wind feed-in premium expired at the end of 2020. In a race to get capacity connected in time, installations more than doubled compared to 2019. Developers used extra cranes from halted industries at project sites, and sent workers to upstream suppliers’ factories to ensure the timely supply of components. Turbine makers increased the number of shifts so that facilities were operating nearly 24/7, while improving component production efficiency.

In the U.S., there was a similar push. Onshore wind tax credits in the country were due to begin a phase-out schedule at the end of 2020. The pandemic resulted in some delays, but most developers were able to get projects back on track and commission before the end of the year. We estimate that an unprecedented 11GW came online in the fourth quarter of 2020. This is more than the annual installation for any year since 2012, the year before tax credits lapsed in the U.S. previously.

While we do not expect onshore installations to hit 2020 levels again until 2030, the events of last year help contextualize future spikes in build. They underline once again the potential influence of subsidies that make or break project economics, and the power of the wind supply chain to flex and rapidly expand production.

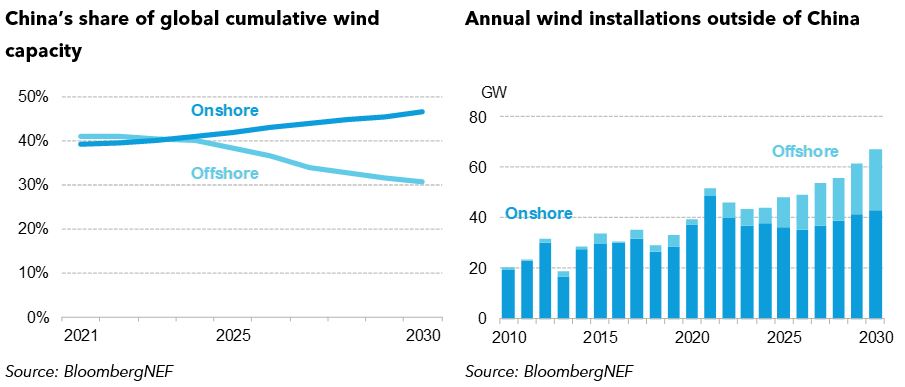

China’s onshore dominance rises, as it falls offshore

China is set to be the powerhouse of global onshore wind addition this decade. From 2025, we predict the country could install more capacity each year than the rest of the world combined. By 2030, China will account for almost half of cumulative onshore wind installed globally (‘China’s share of global cumulative wind capacity’ chart), despite only accounting for about a third of global generation capacity.

China has been able to avoid some of the problems that have slowed onshore wind installations elsewhere, such as local opposition, permitting hurdles or delayed grid rollout, especially in established European markets like the U.K. and Germany. This means China can hit its carbon neutrality goals with a higher share of cheap onshore wind compared to other nations which are turning to offshore development.

Although China is set to be the world’s largest offshore wind market this decade, its share of global cumulative capacity is set to fall over the period (‘China’s share of global cumulative wind capacity’ chart). Governments outside China are increasingly looking offshore. Our forecast shows that onshore wind additions outside China will stay relatively flat in the second half of the decade (‘Annual wind installations outside of China’ chart). The major growth will move offshore, and bring other benefits, like green jobs. However, a reliance on the technology looks set to lock some countries into significantly higher capital costs for the bulk renewables generation needed to achieve their decarbonization goals.

Related Content