This analysis is part of Hyperdrive, a series devoted to the future of cars. It appeared first on Bloomberg.com.

Electric trucks are grabbing a lot of headlines lately. Elon Musk announced Tesla Semis will start shipping to PepsiCo in California. Volvo is delivering battery-powered big rigs to Amazon in Germany.

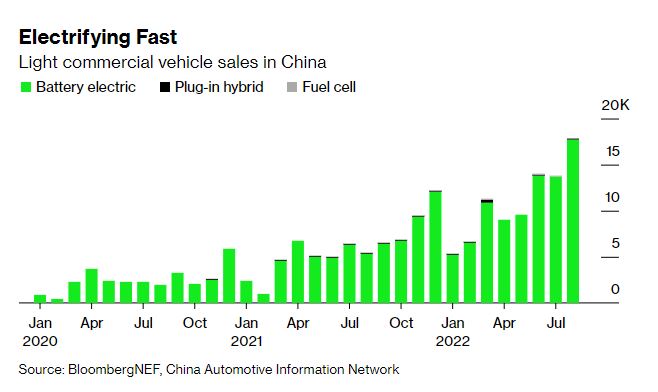

But few markets are electrifying quite like China, where EVs have gone from less than 1% of light commercial vehicle sales to 10% in just the last two years. Sales reached a record high of almost 18,000 in August and look likely to keep rising in the final few months of the year.

China is the largest commercial vehicle market in the world, so what happens there moves the needle globally. At 10% electric share, China is well ahead of almost all other countries in this segment. Only South Korea has a higher adoption rate, with more than 20% of its light commercial vehicle sales already electric so far in 2022.

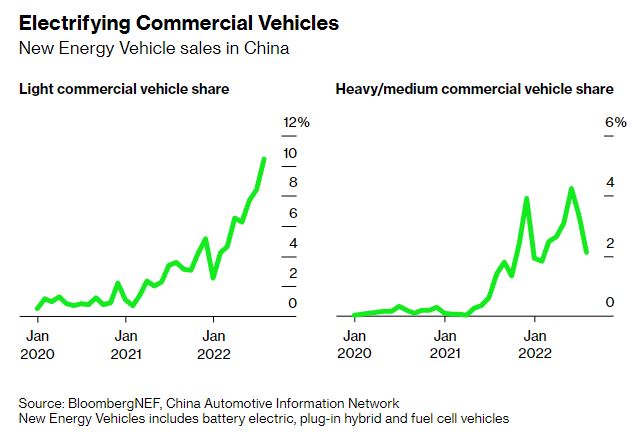

The adoption curve for light electric vans and trucks in China has started to look a bit like what happened with passenger vehicles a few years earlier, when the combination of policy support, more model availability and a surge in charging-infrastructure investment led the market to take off. Momentum has continued on the passenger vehicle side, with plug-in vehicles hitting 29% of all sales in September. Full electrics were 22% of the market.

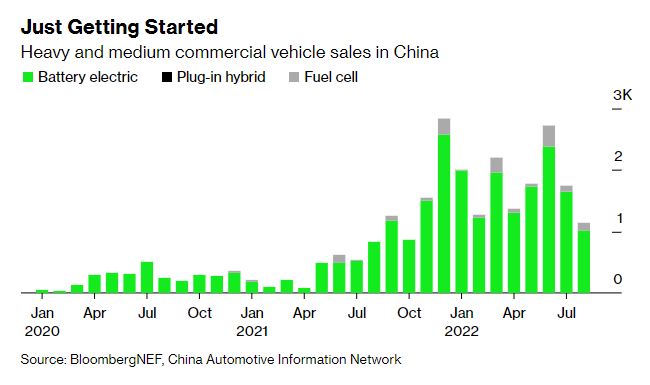

The market for electric medium and heavy-duty trucks in China is also picking up. Sales of electric big rigs in that segment rose 224% in July and hit 3.4% of the total market. Deliveries dipped slightly in August, falling to 2% share, but the trend for the year is still strongly up and to the right.

So far, most of these heavy trucks are operating in shorter-range urban duty cycles, rather than long-haul routes, but the picture is changing quickly nonetheless. It’s easy to be dismissive of a few percentage points of market share, but technology adoption stories have a habit of going slowly, right up until they don’t

Earlier this year, I wrote about how China was experimenting with the right mix of policy, technology and economic levers to drive zero-emission options in these heavier vehicle segments, and that things could move quickly once the optimal mix becomes clearer. That point may be arriving now, and the latest data challenges two widely held beliefs in both the transport and energy sectors.

The first is that hydrogen fuel cells are the main, or even the only, way to clean up heavy trucks. The data so far shows that while fuel cells are playing a role, most of the alternative heavy trucks being sold in China are battery-electric. It’s early days and this could still change, but BNEF analysis indicates that at least for urban duty cycles, electric heavy trucks are already much more economically competitive and will remain so even with the expected decline in the cost of hydrogen and fuel cell stacks.

The last standing area of contention is long-haul trucking. That segment is still up for grabs, but even there, recent BNEF analysis on planned model launches showed a huge divergence between the number of electric and fuel cell trucks coming to market. There are a lot corporate net-zero targets that are starting to filter down to the supply chain in the next few years that will pressure big logistics fleet operators to start getting zero-emission options on the road. Electric models have a serious head start.

China is also experimenting with battery swapping for commercial vehicles, showing there’s more than one way to skin the cat. Data compiled by BNEF shows a 318% increase in the number of commercial battery swap stations set up in China last year, and planned deployment of 34,000 vans and trucks with swappable batteries. A single city, Tangshan, has deployed over 4,400 heavy-duty battery-swapping trucks as of September. That’s more than the entire global heavy duty fuel cell truck fleet.

The other orthodoxy that sales data cuts against is that commercial vehicles will keep oil demand in the road transport sector growing steadily in the decades ahead. Most major oil outlooks now acknowledge that passenger vehicle oil demand has either already peaked or will soon. But almost all of them assume steady growth in demand from the commercial vehicle segment as countries get richer and more freight continues to be moved by road.

In BNEF’s 2022 Road Fuel Outlook, commercial vehicle growth keeps oil demand growing, but not for long. This year’s outlook has overall road transport oil demand peaking in 2027, but if sales of electric trucks continue to rise sharply in China, that could be pulled forward.

Related Content