The next few years are a sink or swim moment for carbon offset markets, which allow for the trading of verified emission reduction credits equivalent to one ton of carbon each. BloombergNEF’s 2023 Long-Term Carbon Offsets Outlook provides a round-up of a turbulent past year for the market, but also forecasts supply, demand and prices under three main scenarios: the voluntary market, removal and bifurcation scenarios. The report paints a bullish long-term outlook if several fundamental issues are addressed, which could value the market at $1 trillion annually as early as 2037.

1. The offset market shrunk in 2022:

Companies bought just 155 million offsets, down 4% from 2021 due to fears of reputational risk from purchasing low-quality credits. At the same time, crypto companies that featured prominently in carbon offset buying in previous years were banned from the largest offset registry in Verra, for fear that they further obscure market transparency through tokenization. Supply of such credits grew just 2% in 2021, with 255 million offsets created by projects in 77 different markets. Investors and the media have taken aim at the quality of credits, specifically in sectors like avoided deforestation, which saw supply tank by 32% in 2022. At the same time, pricing from the suite of new futures contracts created for the offset market plummeted throughout the year. CBL’s nature-based offset futures, which source from high-quality REDD+ and reforestation projects with co-benefits, opened trading at $14.4/ton in February 2022, but have since fallen to $4.6/ton at the end of 2022.

2. Long-term, fundamental demand will set the tempo:

Today’s fluctuating offset demand is mostly classified as behavioral, meaning companies buy offset to differentiate products or satisfy customers. It’s more responsive to prices and criticism, and BNEF expects behavioral demand to drop from 181 million tons (MtCO2e) in 2023 to zero in 2050 in its baseline projection. It will be replaced by fundamental demand as companies work towards net-zero goals, meaning they will need offsets to neutralize any emissions remaining after they’ve reduced their gross emissions. BNEF’s baseline projection has fundamental demand increasing to 1.1 billion tons (GtCO2e) in 2030 and 5.4GtCO2e in 2050. This type of demand is less price elastic and takes over long-term, but hinges on companies sticking to their targets and financials enforcing this among their portfolios.

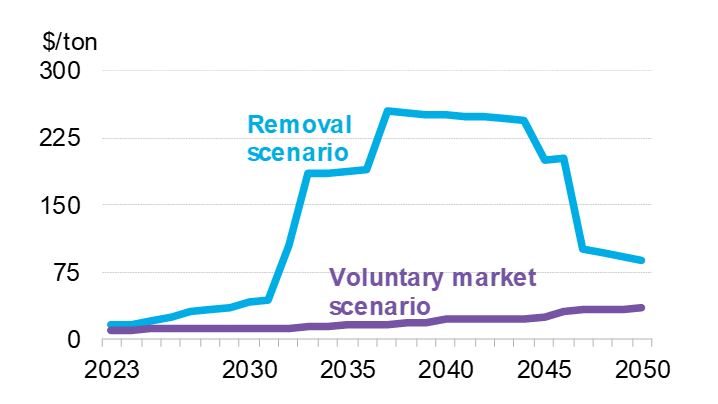

3. The structure of today’s market is unsustainable:

In BNEF’s voluntary market scenario, companies are free to purchase any type of offset they’d like to meet behavioral and fundamental demand, similar to how today’s market functions. This includes full flexibility around sector, geography, vintage (age) and whether the project avoids or removes carbon. In this scenario, supply (4.5GtCO2e) would be almost four times greater than demand (1.2GtCO2e) in 2030 – with avoided deforestation accounting for 64% of credit created. Offsets will cost just $13/ton at that point, valuing the market at a mere $15 billion. Prices rise to $35/ton in 2050 as demand increases from companies needing to achieve net-zero goals. Such an outcome would allow companies to continue to invest in cheap, low-quality offsets while crucial technology-based removal like direct air capture would fail to get needed investment.

4. A removal-only market would send offset prices sky-high:

An alternate outcome is a market where the same companies working towards net-zero goals can only purchase carbon offsets that come from removal projects. This would put more emphasis on nature-based solutions like reforestation and regenerative agriculture, as well as technology like direct air capture, while sectors like avoided deforestation and renewable energy would see their demand plummet. A removal-only market keeps the supply-demand balance skin-tight out to 2050, with the market briefly undersupplied from 2037 to 2044. Prices would rise to a manageable $42/ton in 2030, before shooting up to $105/ton in 2032 and $254/ton in 2037 – valuing the market at nearly $1 trillion annually. While this scenario would grow the market the largest and direct much-needed investment into technology-based carbon removal, it possible that such high prices could alienate buyers or force them to abandon their net-zero goals as they will be too expensive to achieve.

5. Creating a standardized definition of high-

and low-quality is the offset market’s space race:

Groups like the Integrity Council on Voluntary Carbon Markets and the Carbon Credit Quality Initiative, as well as rating agencies like BeZero and Sylvera, are hard at work on this topic. Once created, it’s likely the market diverges into a less liquid, more expensive market for high-quality offsets and a larger, cheaper market for everything else. BNEF estimates that such a market denoted by quality peaks at $38/ton in 2038, but would still be too cheap to incentivize investment into technology-based removal like DAC. A low-quality market would exacerbate many of the issues already seen in today’s market and prices would peak at just $22/ton in 2050. Just how fundamentally different these markets would be is based on how inclusive the definition ‘high-quality’ is. In addition, these competing efforts could ultimately drive more confusion in the end.

Related Content